The productization of services

Over a decade ago, Marc Andreessen coined the phrase Software Is Eating the World to describe a phenomenon that was already well underway:

More and more major businesses and industries are being run on software and delivered as online services — from movies to agriculture to national defense. Many of the winners are Silicon Valley-style entrepreneurial technology companies that are invading and overturning established industry structures. Over the next 10 years, I expect many more industries to be disrupted by software, with new world-beating Silicon Valley companies doing the disruption in more cases than not.

Just a couple of years later, in Consulting on the Cusp of Disruption, Clayton Christensen and team described how this phenomenon was playing out in management consulting specifically:

Scores of start-ups and some incumbents are also exploring the possibility of using predictive technology and big data analytics to deliver value far faster than any traditional consulting team ever could… big data firms are growing explosively, fueled by private equity and venture capital eager to jump into the high-demand, high-margin market for such productized professional services… Only a limited number of consulting jobs can currently be productized, but that will change as consultants develop new intellectual property. New IP leads to new toolkits and frameworks, which in turn lead to further automation and technology products. We expect that as artificial intelligence and big data capabilities improve, the pace of productization will increase.

In this context, “productization” is synonymous with “eating.” It’s the development of software that codifies some process that was previously executed as a service performed by a human. The piece identifies intellectual property (IP) as the driving force behind the productization of services. IP is the result of an investment of time and/or capital. This raises a question - what distinguishes the services that merit the investment for productization from those that don’t? It comes down to Unit Economics. Imagine evaluating every customer need on two dimensions - the value of the market for that need and the initial fixed cost of developing the IP to productize that need. A less economic, more intuitive way to conceptualize this might be the number of instances of that need and the technical complexity of addressing that need. We can make these dimensions axes on a graph and plot some needs. Let’s focus on financial services:

This is pure conjecture. I don’t have any empirical justification for the positioning of any of these needs. It’s just based on my sense of how frequently needs arise and how hard it is to make software to address them.

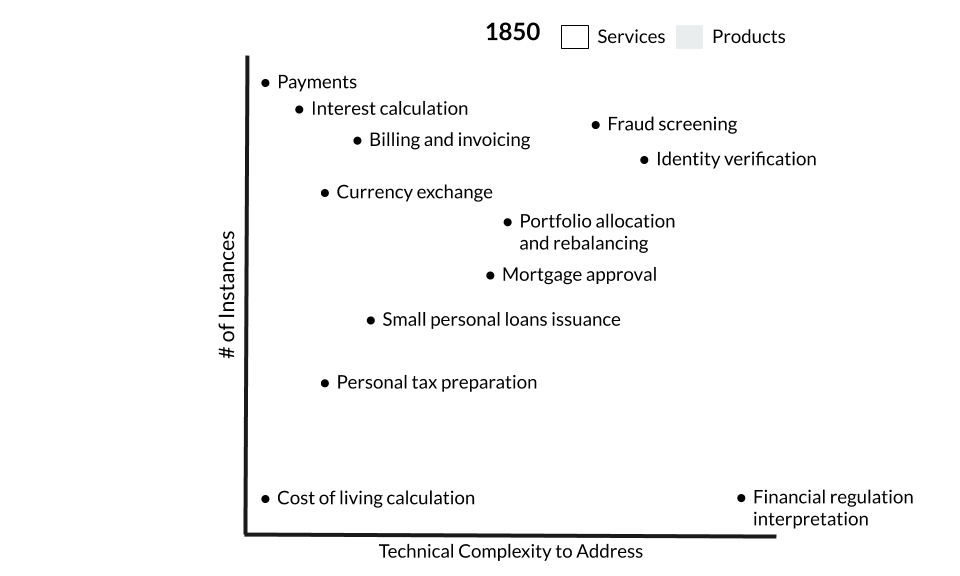

In the top left corner are needs that occur all the time and require very little judgement to address, like payments (excluding the compliance part, which we’ll get to). Humans have been making payments for thousands of years. Bankers have been around for almost as long, facilitating payments as a service. Facilitating payments reliably at scale is a very technically complex challenge, but for our purposes lets consider it the minimum level of technical complexity.

In the bottom right corner are needs that happen rarely and involve a high degree of judgement to address, like the interpretation of financial regulations. There are perhaps a few thousand financial institutions that might need guidance interpreting new regulations each time they are issued. Computers are a long way from understanding financial regulations and their implications for the operations of a business.

We can use this graph to trace the productization of an industry. It wasn’t long ago that every one of these needs was addressed purely via services. The productization of financial services is a recent phenomenon, as Tommy Nicolas explains in his “Thrilling History” of financial services:

The “payments” industry really began with Western Union. Western Union began as a telegraph service in 1851, but in 1871 it introduced a money transfer service based on its telegraph infrastructure.

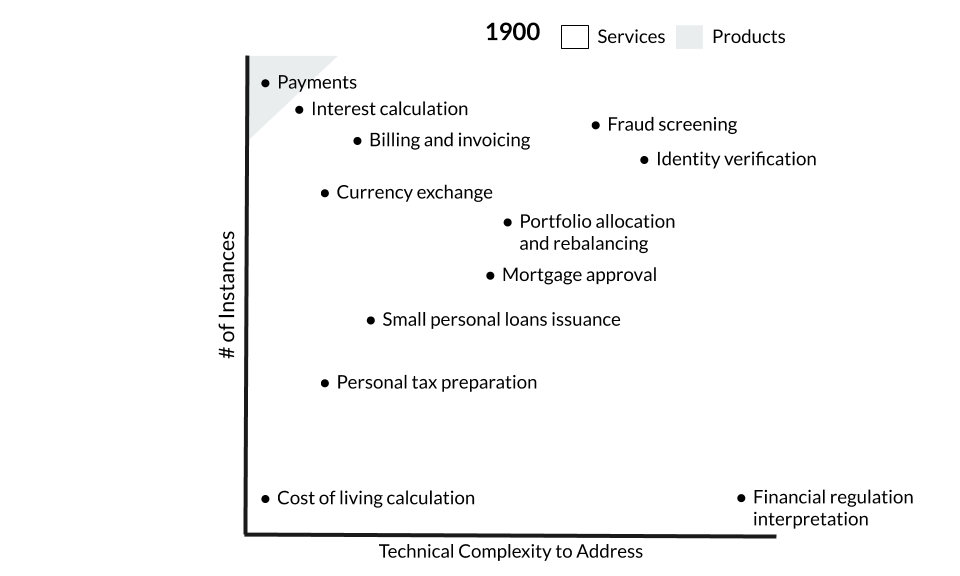

That telegraph infrastructure was perhaps the first of many financial products, kicking off a wave of financial services productization that persists to this day. There may have been no products in 1850, but by 1900, payments had been at least somewhat productized:

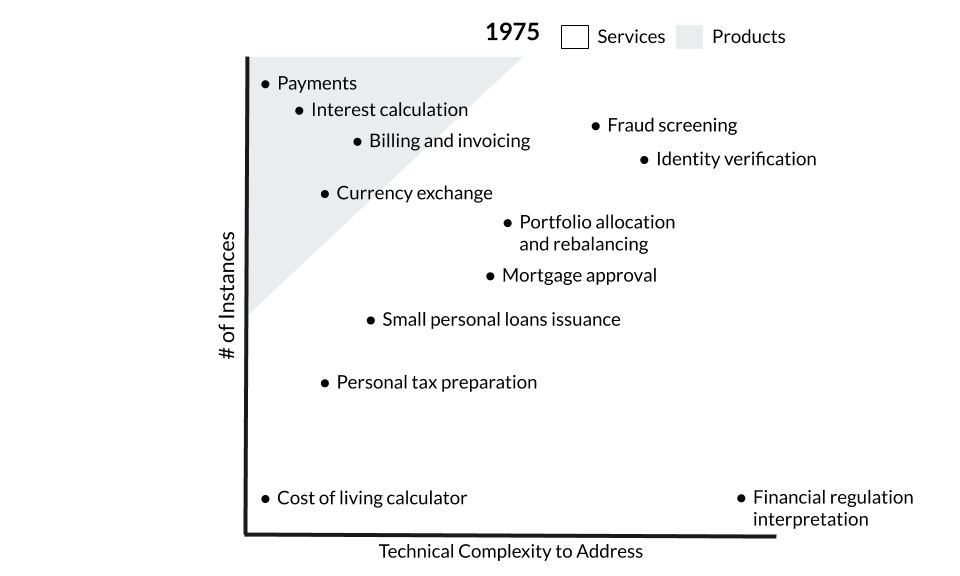

By 1975, more technology innovations, such as the digital computer, had spread such that additional needs could be productized, like interest calculation or billing and invoicing:

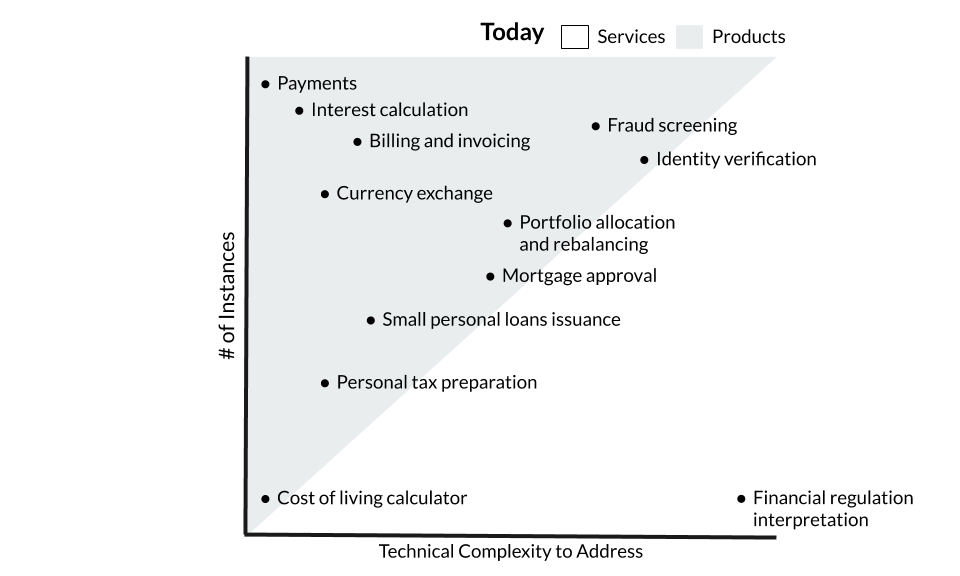

Fast forward to today - technology innovations like machine learning, knowledge graphs, and better interfaces are driving the rapid advancement of the productization line across the graph:

The line represents the “frontier” of technology innovation. Needs just above and to the left of the line are eligible for productization. Products that address these needs compete against incumbent services. Over time, products dominate needs in the top left corner. For now, services dominate needs in bottom right corner. Of course, the line is a simplified representation of a much more complex phenomenon. The reality is much blurrier.